Top eMortgage Trends Shaping the Housing Market in 2026

Top eMortgage trends in 2026: digital mortgages, AI in lending, eClosings, and faster approvals shaping the future of home buying.

How eVaults Are Revolutionizing Loan Storage and Security

The mortgage and lending industry is undergoing a rapid digital transformation, and at the center of this evolution lies a powerful technology: eVaults. Often described as the “digital Fort Knox” of mortgage lending, eVaults are redefining how loan documents are stored, secured, and transferred.

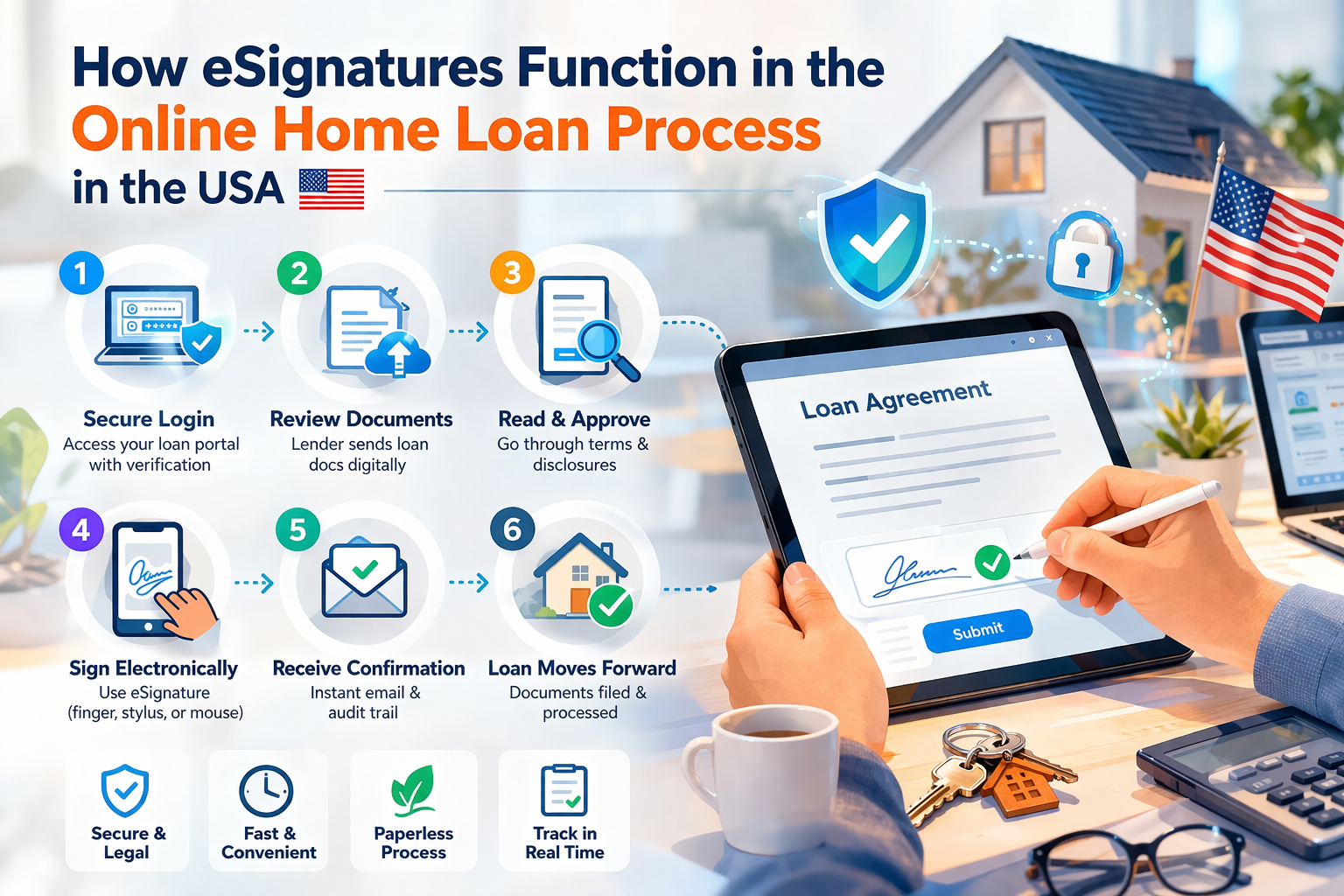

How eSignatures Function in the Online Home Loan Process in the USA

Learn how eSignatures streamline the online home loan process in the USA, making mortgage applications faster, secure, and paperless.

7 Compelling Reasons to Choose a Digital Mortgage Over Traditional Loans

Discover 7 powerful reasons why digital mortgages are better than traditional loans. Learn how they offer faster approvals, convenience, and transparency for modern home buyers.

How First-Time Buyers Can Leverage Digital Mortgage Platforms

Learn how first-time home buyers can use digital mortgage platforms to simplify the home loan process, save time, and secure better deals.

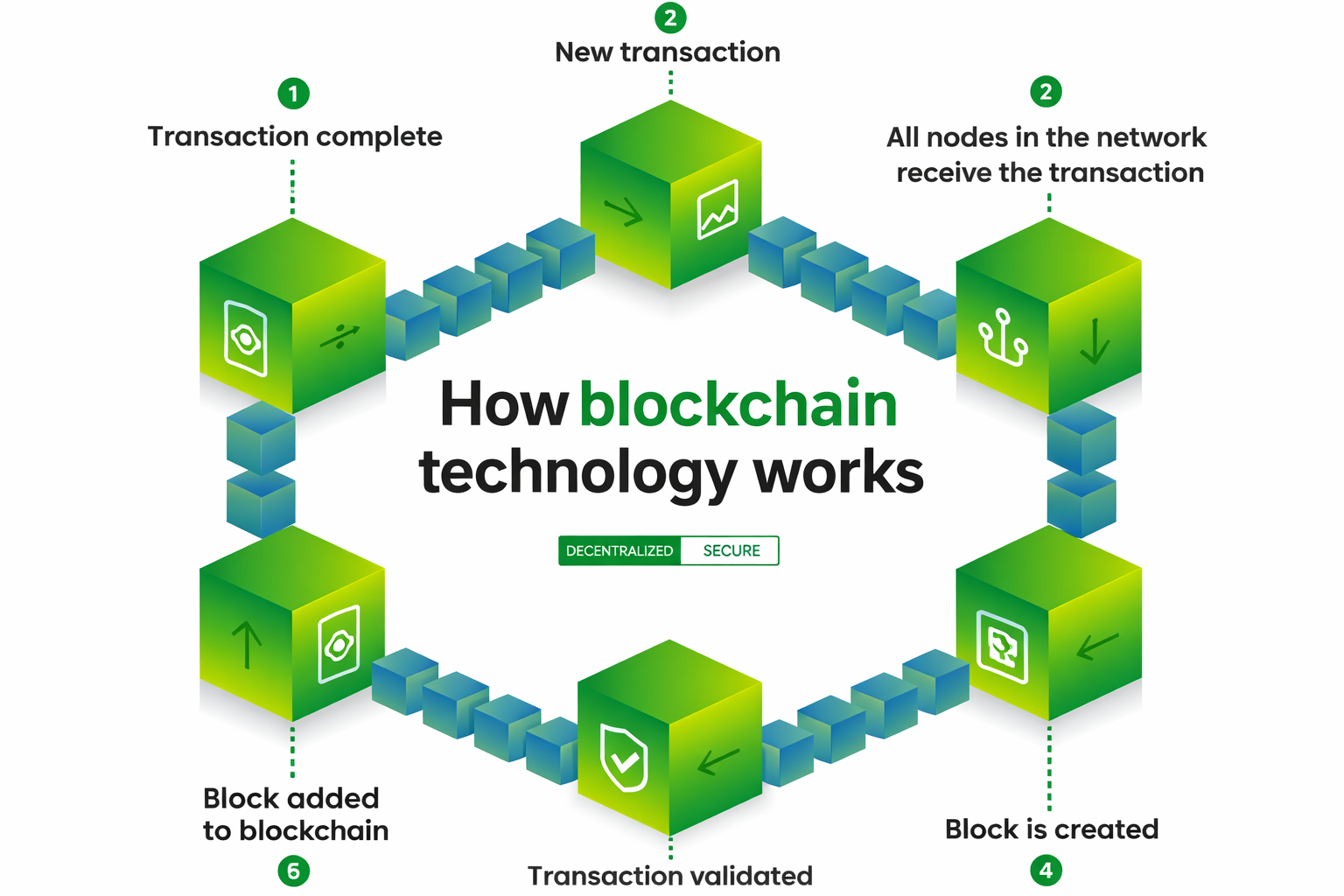

Transforming Mortgage Security: The Role of Blockchain Technology

Transforming mortgage security with blockchain technology—explore how it enhances data protection, reduces fraud, and streamlines lending processes in 2026.

How AI and Digital Mortgage Technology Are Transforming Lending in 2026

Discover how AI and digital mortgage technology are transforming lending in 2026 with faster approvals, eClosings, and smarter home loan solutions.

How to Keep Your Mortgage Brand Strong in Tough Markets: Lessons from CEO Lisa Lund and Joe Shalaby

Joe opens by spotlighting Lisa’s reputation in the space and her leadership as a mortgage executive. Early on, there’s also a fun moment of overlap: Joe mentions his show is called Coffeez for Closers, and Lisa had previously had a show called Coffees with Closers—a small but telling detail that reflects how aligned they are on the idea of learning from closers, operators, and builders.

Building a Mortgage Empire: The Habits, Vulnerability, and Vision Behind Real Growth

We love the highlight reel: production numbers, rapid expansion, big titles, big wins. But the more interesting question is what happens underneath all of that—what someone does daily, how they lead when things feel uncertain, and how they build people and systems that can actually carry the weight of growth.

The Moment: Why This Conversation Hits Different

Plenty of podcasts talk about success. This one leans into the unglamorous parts—how credibility is earned, how teams are built, and how real operators think when the stakes are high.

The Problem With “Entrepreneur” as the End Goal

Nick’s central challenge is simple: the culture celebrates the label “entrepreneur,” but the label alone doesn’t guarantee freedom, wealth, or impact. In his view, the mission shouldn’t stop at starting something—it should progress toward building something that can produce an outcome.

The Big Idea: Learn the Game Before You Try to Beat It

A recurring point in Daniel’s story is that he didn’t rush into big moves until he felt fully equipped. Instead of jumping ahead, he focused on understanding the business deeply enough to serve clients with confidence—knowing he was providing a strong product and a strong experience.A recurring point in Daniel’s story is that he didn’t rush into big moves until he felt fully equipped. Instead of jumping ahead, he focused on understanding the business deeply enough to serve clients with confidence—knowing he was providing a strong product and a strong experience.

The bigger story: success is built in the operating system

A recurring theme in the conversation is that real business performance isn’t just about “working harder” or having a strong quarter—it’s about building an operating system that makes performance repeatable. Joe frames the episode around Nancy’s story because it resonates and inspires, particularly for listeners who want a path they can model, not just motivational soundbites.

The Core Theme: Success That Doesn’t Cost You Your Life

The conversation centers on a question many high performers eventually face: What’s the point of winning professionally if you’re losing personally? David’s message is about balance—not in a vague, feel-good way, but as a deliberate commitment to nourishing “the body, the mind, and the spirit,” while still pursuing excellence.

The big idea: “EZ” doesn’t mean effortless—it means engineered

A recurring theme in the discussion is that “easy” outcomes are usually designed. In lending (and most service businesses), complexity creeps in fast: leads, follow-ups, processing, relationships, marketing, team performance, and the day-to-day operational grind.

Innovating in the Mortgage Industry — Modern Leadership, Scaled Communication, and Building Better Systems

The mortgage industry isn’t just competing on rates—it’s competing on experience, speed, and service. In this episode, Joe Shalaby sits down with Kevin Peranio to talk about innovation, leadership, and what it takes to build an organization that keeps progressing even when the market shifts.

A 19-Year-Old Hit a Billion Views in Six Months—Here’s the Viral Strategy He Breaks Down

Growing online can feel like chasing a moving target—especially when you’re trying to figure out what actually works versus what just sounds good. In this episode of Coffeez for Closers, Joe Shalaby sits down with Justin Ho (known online as “themindsetguyy”), who shares how he built a massive online presence fast—and what he believes matters most if you’re trying to grow in 2024.

Real Entrepreneurship Spirit: Leadership Lessons from Sharran Srivatsaa (Coffeez for Closers)

In the first episode of Coffeez for Closers, host Joseph Shalaby (CEO of E Mortgage Capital Inc.) sits down with Sharran Srivatsaa to unpack what “real entrepreneurship spirit” looks like in practice—especially for people building teams, driving growth, and aiming for meaningful outcomes like major scale or an exit.

Why More Credit Unions Are Adopting eMortgage Tech Than Ever Before

Credit unions are rapidly adopting eMortgage technology to streamline lending, reduce paperwork, and deliver faster, more convenient member experiences. With digital closings, eNotes, and improved compliance, they’re boosting efficiency and staying competitive in today’s digital-first mortgage landscape.

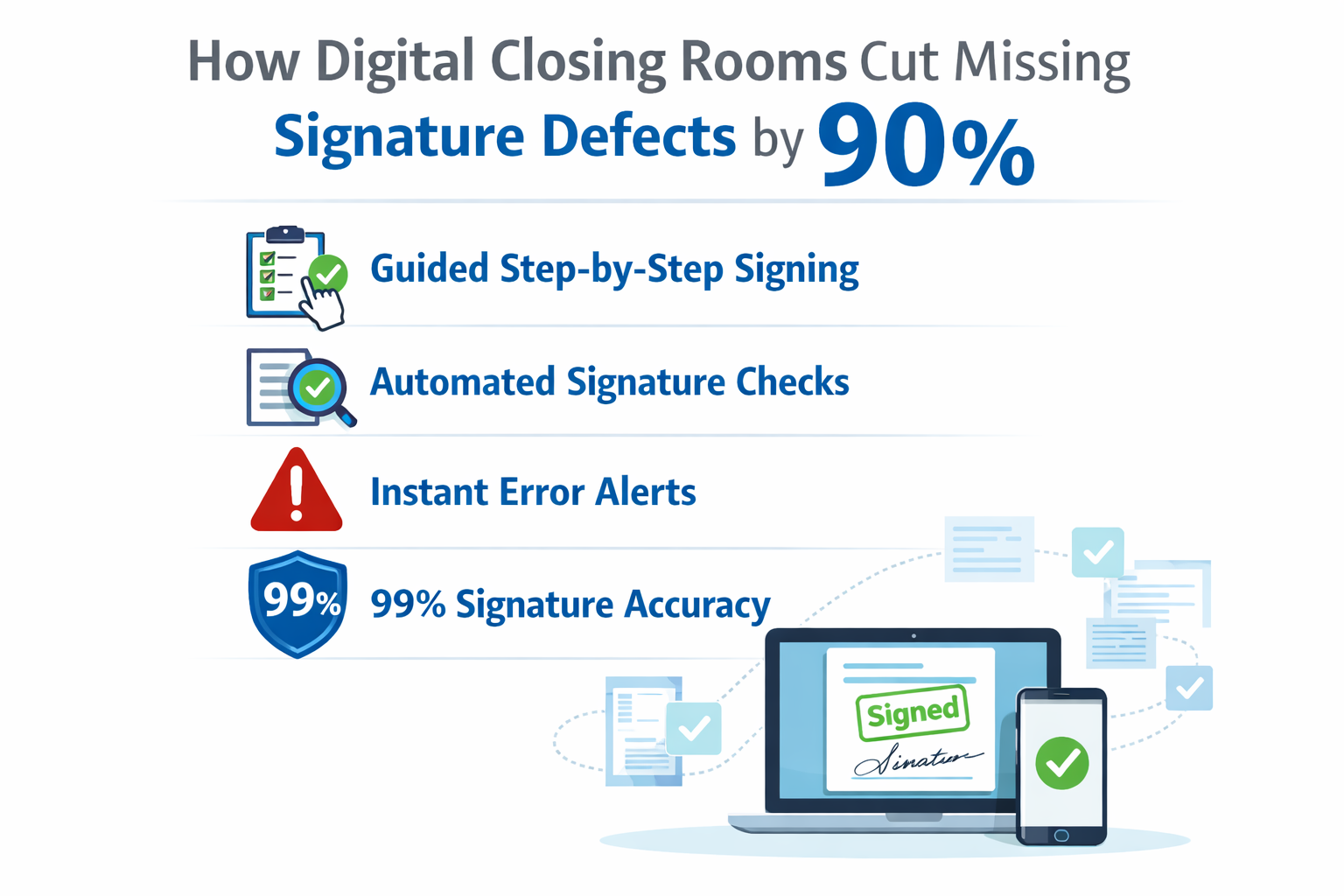

How Digital Closing Rooms Are Cutting Missing Signature Defects by 90%

Digital closing rooms reduce missing signature defects by up to 90% with automation, real-time validation, and smarter workflows that ensure error-free closings.